I‘m Julien Brault and on the show today, how Maxwell Nicholson, CEO and co-founder of Blossom Social, built a social network for investors with over 160,000 monthly active users, 3.8 million dollars in annual revenue and a weekly newsletter that generates 500,000 dollars per year.

Maxwell was making $120,000 a year at McKinsey with a clear path to double that within a few years, but he couldn't shake the feeling that he was meant for something else. He grew up in a small Canadian town called Grand Forks in British Columbia. His dad was a welder and his mom a stay-at-home mom. He and his brother were the first in their family to graduate university.

So, when he landed a job at McKinsey, his grandma thought he was crazy to even consider leaving. But in 2021, at the height of the pandemic investing craze, Maxwell walked away to build a social stock trading app for Canadian investors.

Maxwell Nicholson: I knew that I wanted to leave, so it wasn't too difficult of a decision for me. The senior partner of the McKinsey Vancouver office was actually one of our early investors. So I owe a lot to McKinsey and I loved my time there.

Julien Brault: In 2022, you raised a pre-seed of $750,000 and it included two Canadian stock market YouTubers, Brandon Beavis, who's now a co-founder, and Shay Huang. How did you find them? Because at the time Blossom was not a household name. I don't even know if they had heard about it. So how did you convince people or did they reach out to you? I'm just curious because I do think raising from influencers can create leverage. So I'm curious to hear about that.

MN: Well, Brandon joining the company was a huge turning point for us. I think at that point we had less than a thousand users, maybe less than 10,000. Brandon was really the one that has driven all of our growth to this point. We had reached out to him on LinkedIn because we were just looking for anyone who had “investing” in their bio on Instagram or LinkedIn and just cold messaging them. So we cold messaged Brandon. He hopped on a call with us and then he told us his rates to sponsor a video. We were like, "Wow, we can't afford that. We definitely don't have the money." Then I had another opportunity where a friend of a friend invited me to a barbecue that he was going to be at. I built a more personal relationship with him and sold the vision.

JB: Did he just say, "Okay, I'll do $100,000 worth of media, influencing videos, and you just give me stock?" Or did he actually sign a check?

MN: We were raising our pre-seed round, so Brandon invested $50,000 of his own money. He invested and we granted advisory shares. Over the course of the year, he started driving immense value. I think a lot of other startups might see someone driving all this value and think, "We got him for so cheap, we barely gave him any equity. That's great for us." But for me, I was like, "Wow, there's a huge mismatch in the value he's driving and the equity he received." So I actually had a meeting with him and said, "Hey, we're going to double your equity from the advisory agreement."

He just continued to deliver incredible value and we kept increasing his equity. Eventually the three co-founders had a conversation and said, "Hey, Brandon's basically operating like a co-founder. Let's officially make him one." We had a few beers and I put my arm around him and said, "Brandon, we got to have you on as a co-founder." And he's like, "You better not just be saying this because you're drunk, man."

We had a few beers and I put my arm around him and said, “Brandon, we got to have you on as a co-founder.”

JB: When was that? When did he join full-time as a co-founder?

MN: I think it was pretty early. It was either a year in or a year and a half in. It was probably like six months after that press release you mentioned in 2022. And I'll touch quickly on Shay, the Humble Trader, who's another incredible YouTuber.

The only reason she invested was because Brandon invested. So Brandon and her had sushi together. Right off the bat, day one, Brandon brought in an incredible investor. If that doesn't speak to the early signals of him being an incredible value add to the team, I don't know what does.

JB: You initially started with the social component, a little bit like Robinhood. A lot of people don't know, but Robinhood launched a non-trading trading social media app in 2013.

The plan was eventually to launch a brokerage, a little bit like what Dub is doing today. Then later on you announced that you're happy to be a social network and you don't want the regulatory hurdles of operating a brokerage. So what changed? Because today it's probably easier than ever. There are players like white label, API-driven players like Alpaca that would allow you to basically add this without getting an introducing broker license. So what made you change your mind about allowing trades?

MN: I believe at the time, and maybe it's different now, Alpaca didn't even support Canadian stock trading. So that was a no-go if you're targeting the Canadian market. We sat down and looked at the numbers. If you look at Robinhood's public financial statements, where brokerages make most of their money isn't on equity trading. Equity trading has almost become a loss leader for them at zero dollar commission. They make most of their money on options trading and crypto trading. So even if you can get over the hurdle of the brokerage license, which is maybe a two to three year journey, now you're entering a competitive market with Wealthsimple and Questrade.

Wealthsimple is an incredible product, by the way. Our only differentiation that we really had was that we were going to be a social broker, which in hindsight, I don't think is a true differentiation point to switch someone from Wealthsimple. There's no way in our initial version we're going to be as seamless and simple as they are.

I had told all our investors that we're going to be a brokerage. So pivoting was very hard. I remember calling our investors and saying, "Hey, I don't think this brokerage path is the right path." And they said, "Okay, well, how are you going to make money then?" And I was like, "Well, I don't really know."

I remember calling our investors and saying, “Hey, I don’t think this brokerage path is the right path.” And they said, “Okay, well, how are you going to make money then?” And I was like, “Well, I don’t really know.”

Now, we make a lot of our money through advertising and ETF partnerships. We had some early indications of that, but not enough where I could confidently say, "Hey, we're going to grow from $300,000 to $4 million in two years," like we've done. When we pivoted, that was very unclear. So it was in a sense a very risky pivot.

JB: When you were mentioning the competitive landscape, you mainly mentioned Canadian players. What's the share of your users in Canada versus the US?

MN: At the time we were fully focused on Canada. Then when we pivoted away from the brokerage path and turned into pure play social network, we were like, "Okay, now we can actually be a truly global company." Within six months or so, our audience was 60% Canada/40% US. But I think we're getting closer to 50-50 now. Canada has always been our core market, but we see the US as the next frontier. Obviously there's a way bigger opportunity in the US and that's been a big focus for us over this year and will continue to be over next year.

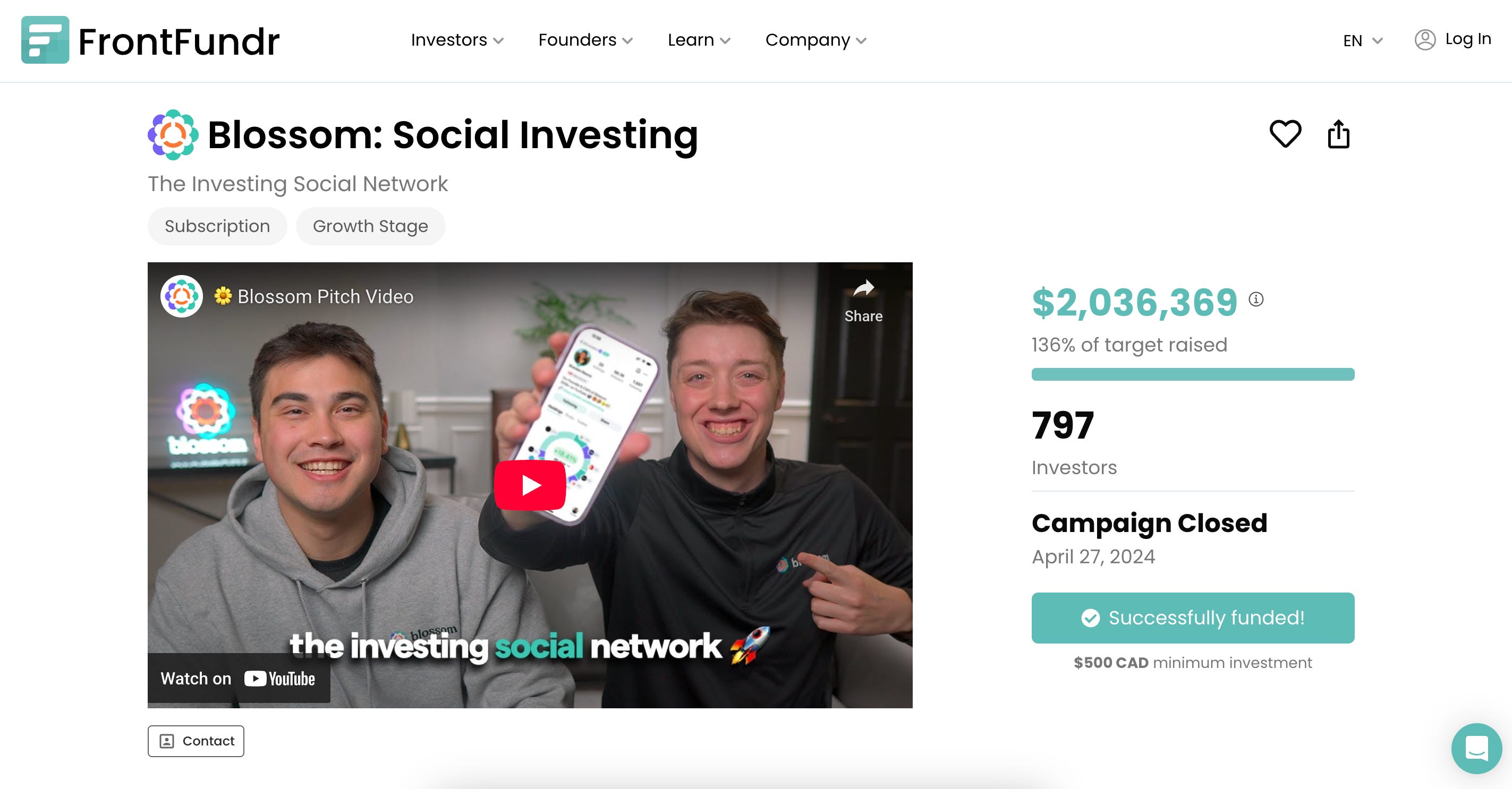

JB: You raised $7 million with a substantial portion of it coming from equity crowdfunding. I actually had a similar experience with my own fintech and I know for a fact it's not an easy path. Did raising money from the crowd become a hurdle or did it actually end up being an advantage?

MN: Having a community of 2,000 super fans is massive. I will send out emails like, "Go upload or repost this LinkedIn post." When we got featured in Forbes, I sent out an email to help boost that. But I think the biggest example of it was our events. So we held an event at the Rogers Center where we had over 1,400 people come out. Probably a good third of those people who came out were shareholders. When you're a shareholder of this company, our event almost has a dual purpose: it's like a conference as well as almost like a shareholder meetup.

JB: Were you charging for the event or was it just for making money?

MN: The event itself was break even. In fact, I think we lost a little bit of money on it. But we charged $60 for the event to cover the cost. Obviously Rogers Center, for context, I think cost us $250,000 to book out. I think they're telling us we might have to pay more next year if we do it there again next year. But yeah, that was epic.

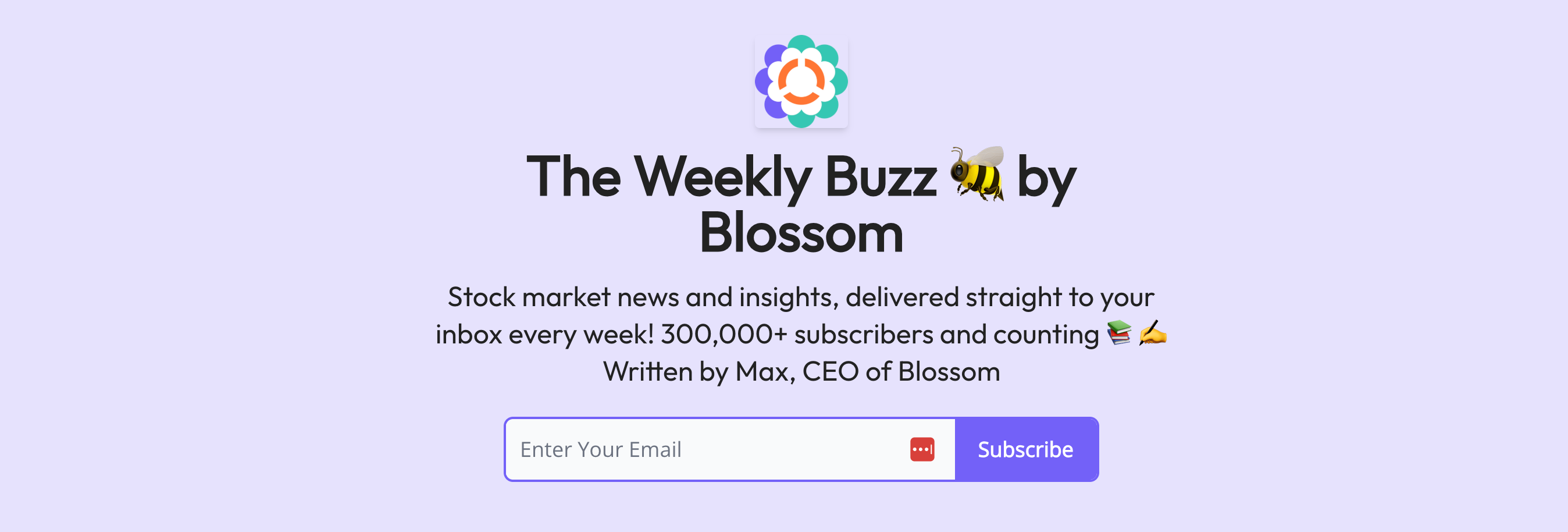

JB: In a recent LinkedIn post, you mentioned that the Blossom newsletter, The Weekly Buzz, is generating over $500,000 in annual revenue on its own. Most fintechs actually have a newsletter, but it's mostly for product updates and re-engaging existing users. How did it become an actual profit center? Can you tell me the story behind this?

MN: The story behind it was two years ago I remember seeing in the news that The Peak sold for $6 million to Zoomer. I remember seeing that and I had seen The Peak's media kit because we had considered advertising in them. So I knew how many emails they had and I was like, "Wait, we have almost that many emails from our users who obviously joined our mailing list and everything." So I was like, "Maybe we can do something like that." And obviously we took inspiration from Wealthsimple TLDR and some of these other great newsletters. So we started really putting time into it, giving a weekly recap of the markets.

Since a lot of our business comes from advertising and partnerships with ETF providers in the app, it was very easy for us to add in newsletter advertising as part of those packages. So I think we do have it easier than other companies, because obviously the sales side of it is the complicated side. If you're just a random fintech, you're not really going to set up a sales team to start selling ads. We were already selling the ads, but it's just given us additional inventory to sell our partners. And the other thing that's really nice about it is that newsletter advertising is very understandable for people. We've had clients where they've started by advertising in the newsletter and then we've been able to shift them to more in-app advertising. But yeah, it's been awesome. I still write it every Sunday, much to my girlfriend's dismay.

JB: Why do you still write it as the CEO of a 30-plus person company? And what do you do differently than other fintechs? Because I think a lot of fintechs, like you mentioned Wealthsimple TLDR, but Robinhood has also invested in newsletters. What's the secret ingredient?

MN: I think the secret sauce is to figure out what your audience actually wants to read. What are they reading and write a newsletter to mirror that with maybe your own spin. The spin with The Weekly Buzz is that it's actually much more like deep dives into a single story versus Wealthsimple TLDR is more high level. We go deep into one story rather than just the high level, which I think makes it unique.

But in contrast, a lot of fintechs or just startups in general are just like, "Here's a product update or here's a sale or whatever." Find out what it is in your niche that people are actually reading and write about that. Because then when you have an announcement, you can just slot it in. I'll slot it into our newsletter as if it's an ad. And the reason that's important is because even for us with the newsletter where we have such a successful newsletter and my open rate on the regular newsletter send is 55-60%. I clean the list regularly, so this 300,000 number is post-cleaning.

JB: So how many active subscribers to the newsletter?

MN: The active subscribers is 330,000. Anytime users haven't opened it in a month or month and a half, I'll just remove them from the list. But what I was going to say was even with that list, when I try and send out a product announcement, Google still sends it to promotions. So Google's gotten so good at telling whether something's promotion or not. And I don't think it has anything to do with the sender. It's like its own algorithm. But if we slot it into the actual newsletter as our own ad, then it will go to the primary inbox. And I know I'm going way into depth on this, but if you go to the promotions folder, it's basically like you may as well have not written the email.

If you go to the promotions folder, it’s basically like you may as well have not written the email.

JB: Apart from the newsletter, how do you make money? You mentioned advertisements, but is it just banners inside the app? Can you explain to me how you actually make money? Because banners are almost impossible to make money on today.

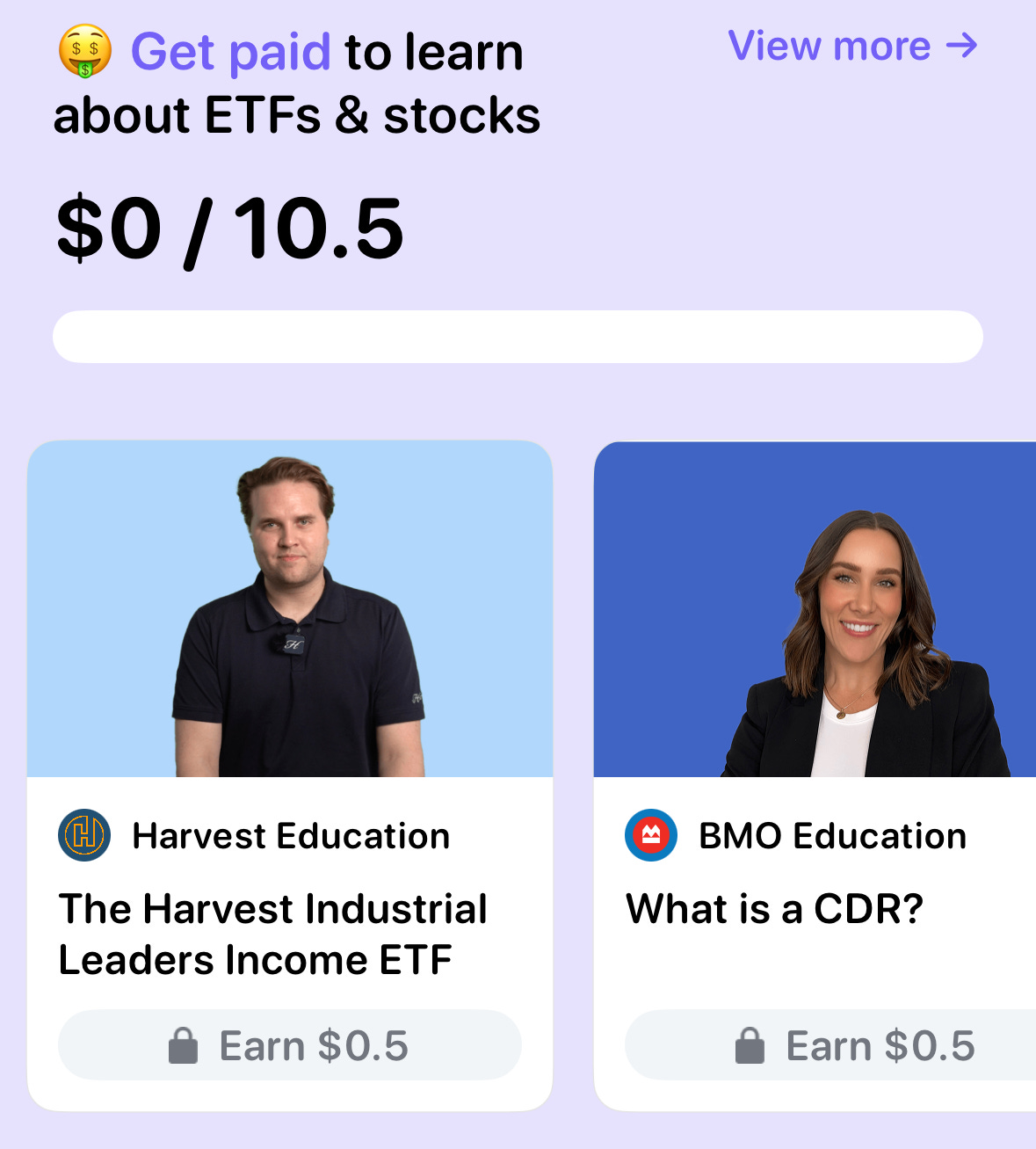

MN: Yeah, they're ineffective and users hate them, right? So I think we've been very thoughtful in how we've built our ad units into the app. One of our core ad units is our “Learn and Earn” section. ETF providers make these short educational lessons about their products. Users can complete the lessons and they earn a small reward.

I wish I could say this was my idea, but I stole that off of Coinbase, which had a similar feature for learning about crypto tokens. I was like, "Why can't we do this with ETFs?" We also have our premium ETF pages, where the ETF providers can basically buy their ETF page in the app and then customize it with their colours and their resources.

JB: That's really interesting because social trading apps are usually about stock picking, but you're telling me a lot of your revenue is actually coming from ETF providers. That's a bit confusing to me because people who just index, let's say the S&P 500, don't really have much to talk about regarding their investing strategy on a social network. So how does that work?

MN: It's a funny nuance about Blossom and it's really tied into our ethos of building the platform for long-term investors. We have about $4 billion in linked assets to the app and 60% of that is held within ETFs. And ETFs and dividends are the most talked about, they're the most followed topics on the app. So we've actually geared the app to be specifically for long-term investors and dividend investors.

We have about $4 billion in linked assets to the app and 60% of that is held within ETFs.

JB: So that's your differentiator with Dub. You're not the Wall Street Bets crowd. You're more the investing crowd.

MN: Yeah, exactly. If you think about the industry, Dub would in my mind fall more in the copy trading bucket. Dub and eToro have social elements, but they're more geared around explicit copy trading. And then you have something close to Dub in the US, which is more of the Wall Street Bets crowd, called After Hour. So all of those, I think, are great platforms, but for a very different audience. If you love Wall Street Bets, Blossom probably isn't the best place for you.

JB: Do you allow your users to monetize and sell access to their trades?

MN: No, and it's for the exact reason we're talking about. A lot of the conversation is more around people learning how to invest, people encouraging each other, sharing milestones, encouraging each other on their journey, rather than me saying, "Hey, I'm the best investor in the world. You should follow everything I do." So we build more of a true community around the app, which I'm very proud of, and more transparency and knowledge sharing, rather than stock picking. And I wouldn't even say stock picking, more like aggressive swing trading. Because we still have people doing stock picking, more like long-term investing, fundamental, more Warren Buffett style.

JB: You mentioned that you wanted to double your user base within about a year. What are your main acquisition channels to get new users in the door right now? I've seen that you're advertising on TikTok and Meta, but I'd like to hear about what's the mix and where your users come from.

MN: Our three main channels are paid advertising. Meta is number one by a fair margin. And then we do TikTok, Google Ads and experiments on other channels as well. We have about 150 finance content creators who are sharing their portfolios on Blossom. And then in any of their videos, they say, "Hey, you want to see what I'm investing in? Come check me out on Blossom." So that's a huge channel. And then, just by nature of being a social network, you have those network effects, people tell their friends.

The paid advertising is the most predictable channel. I think it's the one where I can say with confidence that we will double by next year. Because with consumer apps, as you know, your LTV to CAC ratio is very important. With our paid ads, we hit about on our marginal spend about a 3 to 4x LTV to CAC with less than a one year payback period. So it's very profitable and we're testing probably a thousand different creatives at any time, not a thousand different videos, but Brandon will have five or six different variations of the same video with different text, different targeting. Every time I say this number, he always says that I got it wrong, but yeah, he showed us a slide in our planning where he'll test like 60 different creatives to find one winning creative. So we have that down to a really good science.

JB: And how do you use AI to get there faster?

MN: The most interesting ways that we use AI, I think one of them is even in our moderation. We've built really good AI moderation to tell if something is scammy or promotional, because I think a lot of platforms, maybe they've adapted now, but if you look on Instagram or especially TikTok, you'll still see all these scam comments. And it's often finance scams, right? AI has been pretty good at telling whether that's a scam. We used to play whack-a-mole with keywords. So it'd be like, "Follow Julien Brault on Facebook for all your trades." And you'd get the keyword, but then they'd find all the different ways to spell your name with different characters. So AI is pretty good at that.

JB: I think a lot of fintechs probably want to get in the influencer game. How do you start this? How do you scale this?

MN: One thing that I is unique about our affiliate program is that a lot of companies say "We're only going to pay for a funded brokerage account." The problem, when you're paying for a funded brokerage account, is that influencers have no control over this process. It's not their fault if your funnel is bad. So our view is, let's just pay them for what they basically have control over, which are the downloads. But the other thing I'll say is that influencers in general don't like affiliate deals. So it's going to be very hard if you're trying to convince influencers to do affiliate deals.

JB: Is it purely performance based? It's not like, "I'll pay you a thousand dollars to do a creative and then on top of that X dollars per app downloaded"?

MN: Yeah, for us it is. The way we've done that is by building relationships with a lot of the influencers. About 20 of them have actually invested in the company. The beautiful thing about our affiliate channel is that our product can fit into any of their organic content, which is not generally true for most fintechs. So our call to action can just be "Come see what I'm investing in on Blossom." So Blossom is really just an extension of their social profile.

JB: How much do you pay per download?

MN: We started at $5, which is the same that we give to refer a friend. And then we have a tiered system that as you hit certain milestones, it'll go up. And you can also unlock other perks too. One of our perks is our ambassador retreat, which we're doing in Tulum this year. I don't think this is applicable for most companies because it is quite difficult to get influencers bought into an affiliate program. Me, Brandon and the team, we're friends with many of them now. So I know they hate affiliate programs. One of the things Brandon has done really well is he found up-and-coming influencers who are maybe smaller but on that growth trajectory. That's a really good one to target rather than just going for the biggest ones in your niche. So that's one practical tip I have to give. And then the second is to look at their recent views, their recent engagement and their recent ads. Don't just look at followers. That's not a good way to evaluate an influencer.

JB: I see more and more people using street interviews to promote products and I don't know if it's ads, but I saw you shared a video about Santa Claus asking people how naughty people like Warren Buffett or Sam Bankman-Fried were.

It catches your eye for sure. Do you do ads in this format or is this pure social media engagement?

MN: We've experimented with the street interview format before too. The Santa one, I'd say, I don't think we're running any of the Santa ones as ads. That was more of a fun one. And for the listeners' reference, we did a campaign called Wall Street Santa where our marketing coordinator dressed up as a purple Santa and went to Wall Street. We have a couple good collab videos coming out. We have one with the Einstein of Wall Street. That was more social media engagement, more of just doing something fun and creative, rather than a pure download push.

JB: When you raise venture capital, investors expect a billion dollar exit. Blossom Social has about 160,000 active monthly users, but given the fact that you're only making money on ads and newsletter sponsorships, how do you become a billion dollar company? What's the maximalist version of Blossom if everything goes right in the next 10 years?

MN: The best comparable I'd say is TradingView. TradingView is also a social network primarily for traders. I think they just raised at a $2 to $3 billion valuation. They're a truly global company. So I think that's the next frontier of Blossom is becoming truly global. At our current level, we're doing about $4 million in revenue, 50-50 Canada-US. There's at least a 5 to 10x opportunity in the US by just doing what we're doing. So that will bring us from $4 million to $20 to $40 million in revenue, which already, you know, at a 10x valuation puts you at half a billion. I think within even the near term, there's a lot of potential there.

Pinterest is an $18 billion company. Obviously they're a very successful social media platform, but my open question is, if we can truly be the social network for investing, I would argue that's more valuable than a Pinterest. It's the same with LinkedIn. They built the social network for careers. I'm sure that idea, when it started out, sounded ridiculous. Any niche social network generally sounds kind of ridiculous. And generally it kind of is. If you're doing a social network for dog walkers or something like that, the problem is that the audience isn't that valuable. We're niche compared to Instagram, but we have the most valuable audience. If you look at our average revenue per user compared to Reddit, it's like 10 times higher than Reddit. So we can be a tenth of the size of Reddit and be as valuable.

JB: That was Maxwell Nicholson, co-founder and CEO of Blossom Social. Thanks for listening to my show. Make sure to follow Fintech Growth Insider on your podcast app so you never miss a new episode. And if you're interested in stealing proven growth tactics from your fintech competitors, please sign up to my newsletter at fintechgrowthinsider.com