When Carlos Caro joined Credit Karma in 2016, the company had 50 million members and was generating $500 million a year. By the time he left, in 2020, Credit Karma had grown to 110 million members and nearly a billion dollars in revenue and was sold to Intuit for $8.1 billion.

Carlos was born in Venezuela, and his family relocated to Washington D.C. when he was three years old. The son of two engineers, he was a strong student, and eventually landed a fully-funded scholarship at Columbia to pursue a PHD in economics. But one year into his PHD, he walked away, because the work felt too abstract. He worried he’d spend his career writing papers that only a handful of peers would ever read.

After a year spent playing pro poker, a high school friend convinced him to apply to Capital One. The process included no less than 9 interviews, and a lot of hard questions, but Carlos got in. There, he encountered a data-driven culture that would prepare him for his role at Credit Karma more than any other.

Carlos Caro: There are executives who lead based on intuition and gut feel. There are very few of those at Capital One. Everyone’s belief is grounded in real data. If they believe something with conviction, it’s because they’ve seen a result that says this is how the world works. There’s a culture there to challenge, doubt, and pressure test everything. As a senior executive, you can’t get away with a point of view that isn’t grounded in reality.

When you made a decision, and I was responsible for many of these, they’re called credit decisions internally, there was a rigorous deck that explained what we’re doing, why we’re recommending it, and then a sensitivity analysis of all the possible outcomes. We’d lay out a pessimistic, optimistic, and base case, and each scenario was pressure tested and standardized.

Julien Brault: Capital One has long positioned itself as an option for people with bad credit. How do you avoid negative selection in that model, where you end up attracting only the people everyone else already rejected? And what did you do on the customer acquisition side to mitigate that risk?

CC: That’s probably one of the keys to Capital One’s early success. I don’t think they started with a website and a TV ad saying “we have subprime cards, come find us,” because that might have attracted exactly the negative selection you’re describing. But if instead you go to the credit bureaus and say you want to look at their data and mail people that fit a certain profile, now you’re proactively getting in front of the user you think is going to perform. You’re avoiding a lot of the risk of attracting unwanted attention. Capital One was very good in the early days at leveraging targeted channels like direct mail.

Over the years, as their brand matured and they expanded into prime products, they got more comfortable making their products open for public application. But I would still guess a very healthy fraction of their book is direct mail and targeted affiliate channels like Experian, Credit Karma, and others that allow you to target based on credit profile.

JB: You joined Credit Karma in 2016, when the credit card business was already doing $500 million a year. Were you walking into something that just needed scaling, or did you have to figure out how to get from $500 million to $1 billion?

CC: The business was cranking when I joined, for sure. I relocated from DC to San Francisco for the position. What I quickly noticed when I looked around was that the results and performance of the business had outgrown its staffing, at least in my functional area of partnerships and business development. I saw opportunity everywhere. I saw the opportunity to do more business with existing partners, to bring on more partners, and to do more innovative things. Lightbox was one example of that.

JB: I have a question about Lightbox. What was it?

CC: Lightbox is essentially a targeting platform for marketers. It enables a marketer on Credit Karma to determine the eligibility criteria for who sees their ads. What Karma was solving for with Lightbox was to drive up approval rates. I remember the CEO being very clear that he wanted approval rates to be 100%. So anyone who applied for a product on Karma should get it. In practice they’re not 100%, but they’re very, very high.

The reason they’re not at 100% is that the data issuers have and the data Karma has to make decisions can be slightly different and refreshed at different dates. But the rate is extremely high. That was one of the big initiatives that, when I looked around, we just didn’t have enough people to execute on. A lot of my job during my four years was to hire the right team.

JB: As VP of Credit Cards at Credit Karma, what was the scope of your role and what was your main KPI?

CC: My KPI was top line revenue. The scope was to manage all the lender partnerships. At the time, Karma’s sole source of revenue was lender partnerships. We were essentially a media seller. These lenders wanted to advertise on our platform and we sold media to all of them.

JB: So you were focused on cards specifically?

CC: Yes, I was on the card side, though at the time we also had a personal loan business, an auto refinance business, and an insurance business. My job was to make sure our lenders felt good about the ROI they were getting on the platform. What usually happened is they would come back asking for more and more. They wanted the growth, and then our marketing and engagement team would have to do the hard work of finding more Credit Karma members so we could serve the demand from the lending side.

JB: Not long after you joined, Credit Karma entered the Canadian market in 2016 and then the UK market in 2019. Those markets already had established credit monitoring apps. How did Credit Karma differentiate itself there?

CC: I’ll caveat this with the fact that I was very focused on the domestic business. But what I observed is that we more or less migrated the same playbook from the States. In the US, the free credit score was the hook to get people to register, ongoing monitoring was the hook to get them to come back, and monetization was the lender ads on the platform. It was more or less the same playbook in Canada and the UK.

JB: At the time, what was driving Credit Karma’s growth?

CC: Our secret sauce was brand marketing. They started doing some experiments on YouTube and programmatic TV. There was an ad they recorded very cheaply, something like $50,000, that started to move the needle on web traffic. And then they just kept leaning into brand marketing. That was one of the bigger drivers for membership.

JB: When did they make that shift toward brand marketing?

CC: That was around 2012. There was a real inflection point after they figured it out. The shape of the growth curve really hit an inflection point after that.

JB: You mentioned Lightbox earlier. Was the goal to increase revenue per member? What was its impact on the business?

CC: It was really designed to drive better outcomes for all three constituents of the marketplace. No one likes to shop for credit card offers and then get declined. That actually runs counter to Credit Karma’s mission, which is to help people make financial progress. If they’re encouraging someone to apply for a product and that person gets declined, it actually hurts their credit score. From the lender perspective, operational costs go way down the higher the approval rate is, because they have costs tied to website maintenance, credit bureau data, and a bunch of other things they pay for on a per application basis. So the higher the approval rate, the better off they are from a cost perspective as well. When we launched the business we were really keyed in on measuring outcomes across all three constituents: is Credit Karma growing, are customers getting a better experience, and are lenders achieving a lower cost of acquisition? We found all three to be true.

JB: I’m curious about this, because if you look at the numbers, in 2016 it was 50 million users generating $500 million in revenue. When it sold to Intuit, it had 110 million users and about a billion dollars in revenue. The revenue per user was flat or had diminished over that period. Why do you think that was?

CC: It’s a really good question. Those comparisons are hard to make, but I think it’s the right math to calibrate on, like a yield-per-user metric. I would suspect if you continued to draw that curve past 2020, the picture would look different. A couple of things to consider: Lightbox was still fairly early in its maturity when Intuit acquired the business. The very first year it launched was 2017, and the acquisition was early 2020, so Lightbox had only really been in the market about two years. The penetration rate across the industry was actually still fairly low. I would say the majority of issuers had not yet adopted the technology. Right now I think it’s at maturity, so if you did the same math today, you’d likely see a different result.

JB: During that period, what was the definition of a “member”? Was it a monthly active user?

CC: It was a consumer who came to the app and was a verified, credit-active consumer with the credit bureau. You had to go through identity verification, and the bureaus had to match you against a record in their database. So it wasn’t enough to just be a real person.

JB: So they may not have been active, but we knew they had checked their credit score at least once. During the period you were there, Credit Karma launched new products like tax filing, insurance, and mortgage. Was this a way to get more data on the user? How did it fit into the business?

CC: The tax move seemed entirely connected to the mission of financial progress, and I think Intuit still thinks about it that way, because they do a lot of cross-promotion between TurboTax and cards. Some very high percentage of consumers, maybe around 50%, don’t have $400 saved in an emergency fund.

When we looked at the tax business, for us it was a way to actually create some of that liquidity for our members, because most Americans’ biggest one-time windfall is actually their tax return. Most people overpay and then get back $500 to $1,000 when they file. The idea was to be there at the moment people filed, not only to help them file, but so that when they got the return, they could make smart use of it. Maybe use it for a secured credit card to improve their credit.

The other part of the story, which maybe isn’t talked about enough, is that the product was 100% free. No upsells. If you’ve used some of the other “free” products out there, you’ll notice they charge you something when you need to file for your state. Karma’s product was totally free, all in the spirit of creating financial progress for people.

JB: You left a few months after the Intuit transaction for $8.1 billion was announced. Did you make some money with your stock options?

CC: Yeah, I did. There were some options there. It’s always nice to feel like you got a little extra in return. I always felt like Karma paid and compensated people very fairly, that was one of the things I loved about working there. But having an exit is always icing on the cake.

JB: Why did you decide to leave Credit Karma?

CC: It had been a little more than four years of working really hard, because the business was being prepared for some kind of exit. I wasn’t in the very small group of executives that worked on the deal with Intuit, so I could sense the pressure and intensity without fully understanding the reason for it. I could feel it in my hours, in how much I was traveling, in the scrutiny when we missed a KPI. Had I known we were being prepared for a sale, I would have understood that a little better. But in retrospect, all startups are like that. Karma was founded in 2007 and the exit was 2020, so that’s a 13-year journey to the liquidity event. I just happened to join in that last four-year sprint. I was tired and a little burnt out. And candidly, the prospect of working for a multi-billion dollar company at the scale of Intuit wasn’t going to be for me long-term, because I’d worked at Capital One as a mega company and my DNA is a little more wired toward act first, ask questions later. I like smaller companies for that reason. When I left Karma, I wanted to start a business. In retrospect, I think I could have stayed two or three extra years, because according to friends I have inside Credit Karma, the culture didn’t really start to change for several years after the acquisition.

JB: Six years later, membership went from 110 million to 140 million, so growth really slowed down. Is that market saturation for credit monitoring apps?

CC: Their revenues have actually grown pretty steadily through the post-acquisition period. But I think you’re pointing at something different, which is membership. I was always a little worried about this, even when I was there in 2016, because there are only about 200 million credit-active individuals in the US. Some people are immigrants who don’t yet have a credit file, some are too young. So there’s a theoretical max audience. It would make sense that at some point there’s an S-curve where rapid growth flattens out. My guess is they’re just in the maturity of that cycle. Their brand is probably as strong as ever on the consumer side. Even now, when I ask people what they use to monitor their credit, I often hear Karma as the number one answer. Although there is a close competitor now in Experian, because they’ve leaned into their marketplace and have real scale there as well.

JB: After leaving Credit Karma, you launched a newsletter called The Free Toaster, and then a marketing agency called New Market Growth. Are there growth strategies you learned at Credit Karma that you now teach your clients?

CC: Yes. One thing that was very notable when I was at Credit Karma was that the lenders who tended to do the best fell into a few patterns. One pattern was a lender that came in and served an audience nobody else wanted. That was almost always a success. For example, a subprime card issuer targeting a highly risky segment that generates above-average losses, but finding a way to underwrite that customer through a security deposit, cashflow data, or by connecting the product to a payroll account.

There are certain audiences that are too risky to lend to on an unsecured basis, but if you secure the product in the right way, you can actually serve populations that don’t have access to credit at all. And if you can be the first mover to deliver that on Karma, you can get outsized rewards. A second pattern is doing the same thing as everyone else, but with very low marketing friction. Your application process is excellent, your approval rates are high. When Credit Karma’s algorithm runs, your offer is viewed as the most efficient and rises up in the rankings.

A third pattern is genuine innovation, doing something fundamentally different or better than everyone else. The Chase Sapphire Reserve launch is a good example.

Chase made a concerted effort to challenge the Amex Platinum, which had long been the go-to card for elite travellers. Chase came out with the same annual fee but packed it with benefits and a 100,000-mile sign-on bonus worth about $1,500 in travel. It was a compelling offer the market hadn’t seen in a long time, and that kind of product tended to perform very well on channels like Karma.

JB: That brings me to a question I’d like your opinion on. I used to run an affiliate publisher, and one of the things I thought was a good idea was asking credit card issuers to give me a better welcome bonus in exchange for a lower commission. How should affiliate managers at fintechs think about balancing those two levers when the total customer acquisition budget is fixed?

CC: This is really tricky. Let’s create a tangible example. Say the card issuer pays you $300 per conversion and they’re offering a $100 bonus to the customer. You’re describing a world where the bank pays $200 to the publisher instead of $300, and $200 to the customer instead of $100. The total spend is the same, they’ve just redistributed how it gets paid. I’ve seen instances where the publisher is better off when that happens, and instances where they’re worse off. It tends to be a function of how well the bonus is promoted and who you’re getting it in front of.

There’s a sweet spot where you can drop your payout a little as the lender, give some back to the consumer, and everybody wins. But that requires a lot of iteration and testing. I’ll give you a recent example. A client ran a test comparing a zero dollar sign-on bonus, a $50 sign-on bonus, and a $100 sign-on bonus. My instinct was that $100 would beat $50 easily. But the result showed the $50 bonus captured most of the response benefit. Their initial response rate was around 2%. With a $50 bonus it went to 3%, a 50% lift. But from $50 to $100, it only moved from 3% to 3.1%.

This was a deep subprime audience that wasn’t used to getting any bonus at all. Once they saw $50, that was compelling enough. The difference between $50 and $100 barely moved the needle. The issuer would have been throwing away that extra $50. So their ongoing strategy is $50. But they wouldn’t have learned that without testing. I don’t have generic advice that unlocks this for publishers universally.

JB: Some credit card issuers are scared of welcome bonuses because they don’t want to attract churners, people who just take the sign-up bonus and cancel the card.

CC: I got that question a lot from the big players. “How can you guarantee that if I get a customer on Karma, they won’t churn onto some other product a year later?” We were never able to guarantee anything. That was just a reality.

JB: Is churning a significant cost, or is it a small population and a cost of doing business?

CC: I actually think it’s a valid concern. I’ve seen publishers that say, “if you have these two products, you should cancel them and get this other product instead,” directly encouraging churning behaviour. There are issuers that will refuse to work with a publisher that does that. It’s going to capture some baseline churn, but that publisher is actively encouraging the behaviour, and that rubs issuers the wrong way.

That said, in practice it’s usually a small percentage of users and, for those users, it is a cost of doing business. But issuers have gotten much smarter about it. I apply for a lot of cards, partly because I enjoy the bonuses but also because I like to experience products firsthand. I’ve been declined for products where the reason given was that I’d already received a bonus on that issuer’s product before.

I noticed Amex handle this particularly well. They said I was approved, I could get the card, but they couldn’t offer me the sign-on bonus because I had received one on another of their products too recently. They didn’t decline me flat out. They said I’m qualified but they can’t justify paying a bonus again. More and more issuers are building systems and policies to defend themselves against this.

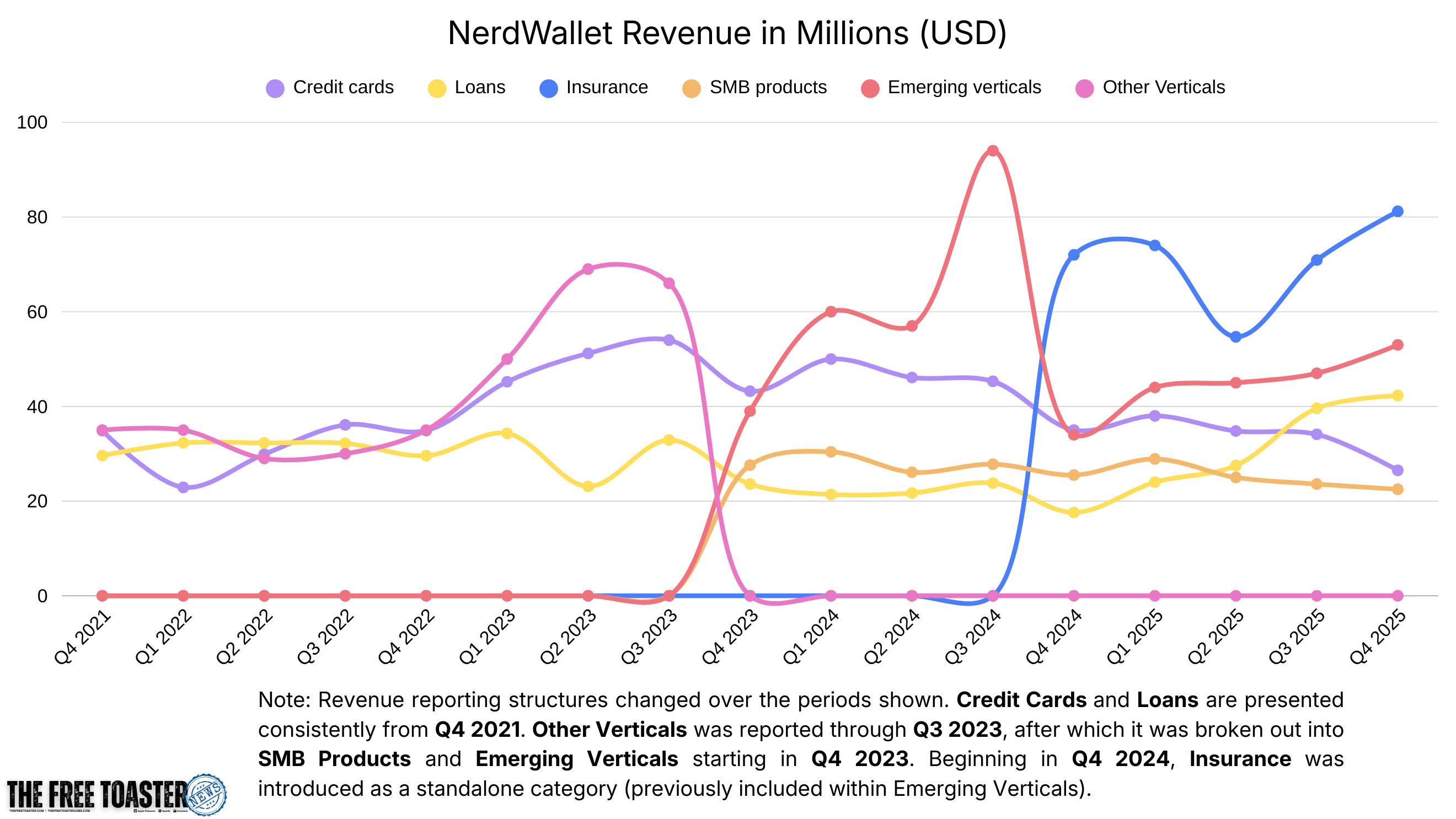

JB: You recently wrote in The Free Toaster about the shrinking credit card business at NerdWallet. It’s not just them; a lot of affiliate publishers are shrinking. What channels should fintechs that want to grow fast be looking at?

CC: To add some colour to NerdWallet specifically, that situation is happening because their SEO traffic has been taking a hit. They even admit it in their earnings, and they’ve announced they’re investing more in paid media, paid social, and paid search to replace the organic traffic. That’s a very different ballgame because organic traffic costs you far less than paid. They’ll have some challenges adjusting to the new normal. As for the channel mix I normally see across fintechs: it’s fairly heavy in direct mail and affiliate marketing. When you roll up Karma, Experian, LendingTree, Bankrate, and the rest, affiliate marketing tends to account for about 40% of account generation. Another 40% is direct mail.

JB: Direct mail seems like a strategy from the 80s. Is it still actually working for fintechs?

CC: I’ve worked with 12 lenders at New Market Growth, and I can only think of one that hadn’t either tested or had a rollout program in mail. And these are predominantly fintechs. I actually hosted a dinner in New York last week where the topic was direct mail, what’s going on and what’s working. Sixteen executives from 11 different companies showed up to talk about it. It’s very much not dead. It’s about 40% of most fintech books. The remaining 20% is some mix of paid search, paid social, and maybe a little brand. Most lenders are underinvested in brand and social. I talked to a VP at a well-known, publicly traded fintech that’s been around since the early days, and he told me brand and influencer marketing is a really big part of their strategy. Most fintechs are under-penetrated there.

JB: Would you say direct mail is actually working better today? I’ve never received so much email, but I get very little physical mail anymore.

CC: The number I most recently heard was that $2 billion per year is spent on direct mail advertising in consumer lending alone. The affiliate category is larger, somewhere between four and six billion, but direct mail is very much alive. And I have a counterintuitive prediction: I actually think AI might create a renaissance for direct mail. Digital advertising is going to get way more competitive because everyone is going to have a bot or an agent running digital ads. It’s going to get really crowded and competitive because you can just automate it away. And then people are going to start looking at direct mail again with fresh eyes.

JB: That was Carlos Caro, former VP of Credit Cards at Credit Karma and founder of New Market Growth, a marketing agency specialized in affiliate marketing in the lending space. Thanks for listening to my show. Make sure to follow Fintech Growth Insider on your podcast app so you never miss a new episode. And if you're interested in stealing proven growth tactics from your fintech competitors, please sign up to my newsletter at fintechgrowthinsider.com