Edoardo Moreni grew up in Rome in a family that was not exactly entrepreneurial. His mom worked at an airline and his dad for Italy’s post company. And while they were always supportive of his ambition, they were mockingly calling him by the nickname of CEO since he was 14.

As a teenager, the future CEO of Emma watched The Social Network 25 times and felt inspired to build something in tech. That’s the reason he ended up enrolling in the computer science program at the University of Manchester in the UK.

Once in Manchester, Edoardo met his co-founder and current CTO of Emma, Antonio Marino, who happened to be the only other Italian in his computer science program. They knew they wanted to start a business together, but they didn’t know what to start.

In 2017, they ended up moving to Berlin to join an accelerator program and launch a peer-to-peer lending company for the German market. It was called Vickiria, a term that the two Italian speakers did not know sounded like “ficken”, the verb “to fuck” in German. They quickly pivoted and launched a German-focused budgeting app with a less offensive name, Kyria. Despite all their effort, Kyria only had about 400 users when they shut it down.

Then the pair went back to Italy to live with their respective parents. Once in Italy, they rebuilt their budgeting app for the UK market and launched the Emma app in 2017. Within 12 months of launching, they had managed to generate 100,000 downloads with zero marketing spend.

Julien Brault: How did you manage to hit 100,000 downloads in your first year without spending a cent on marketing?

Edoardo Moreni: At the beginning, we were refusing to spend money, which I think was probably the right call, because the app was entirely free and we didn’t have much budget anyway. We also went to some of the events that the community organized, and that started driving a significant amount of traffic. We did the same with Starling Bank, which was another new bank coming up at the time. Then there were also a lot of online forums and communities.

Budgeting is something people tend to talk about, so there’s always been a strong organic base. It’s not as strong as a social network, where everyone who joins invites other people. With a budgeting app, if you download it and start using it, you don’t need your friends there too. You can definitely grow it organically for a long time, but eventually, if you want a certain scale, you need something else.

JB: Retention was our biggest challenge when I was running a budgeting app called Hardbacon in Canada. Bank connections would break all the time and getting people to reconnect was brutal. How did you solve retention, and was open banking a game changer for you?

EM: We started pre-open banking, so we had the same issues you had, where it was mostly done by web scraping. After we moved to open banking, we saw a huge amount of people willing to connect with no effort. Connecting the bank is still the biggest drop-off point in onboarding, but it’s nowhere near as big as it used to be. Pre-open banking, I remember we’d lose 50% of people right at the connection page. Now that drop is much, much smaller.

We don’t have those retention challenges anymore, but obviously we still use gimmicks to keep retention healthy. The very first one we added was the daily balance notification. Every day at 8 a.m. you get your balance pushed to your phone. That’s a very Emma-specific feature we introduced in our first year, and it increased retention quite a lot. It creates a pattern of coming back and checking.

JB: For people who don’t know Emma, can you describe what Emma was during that first year, when you hit your first 100,000 downloads, compared to what Emma is today?

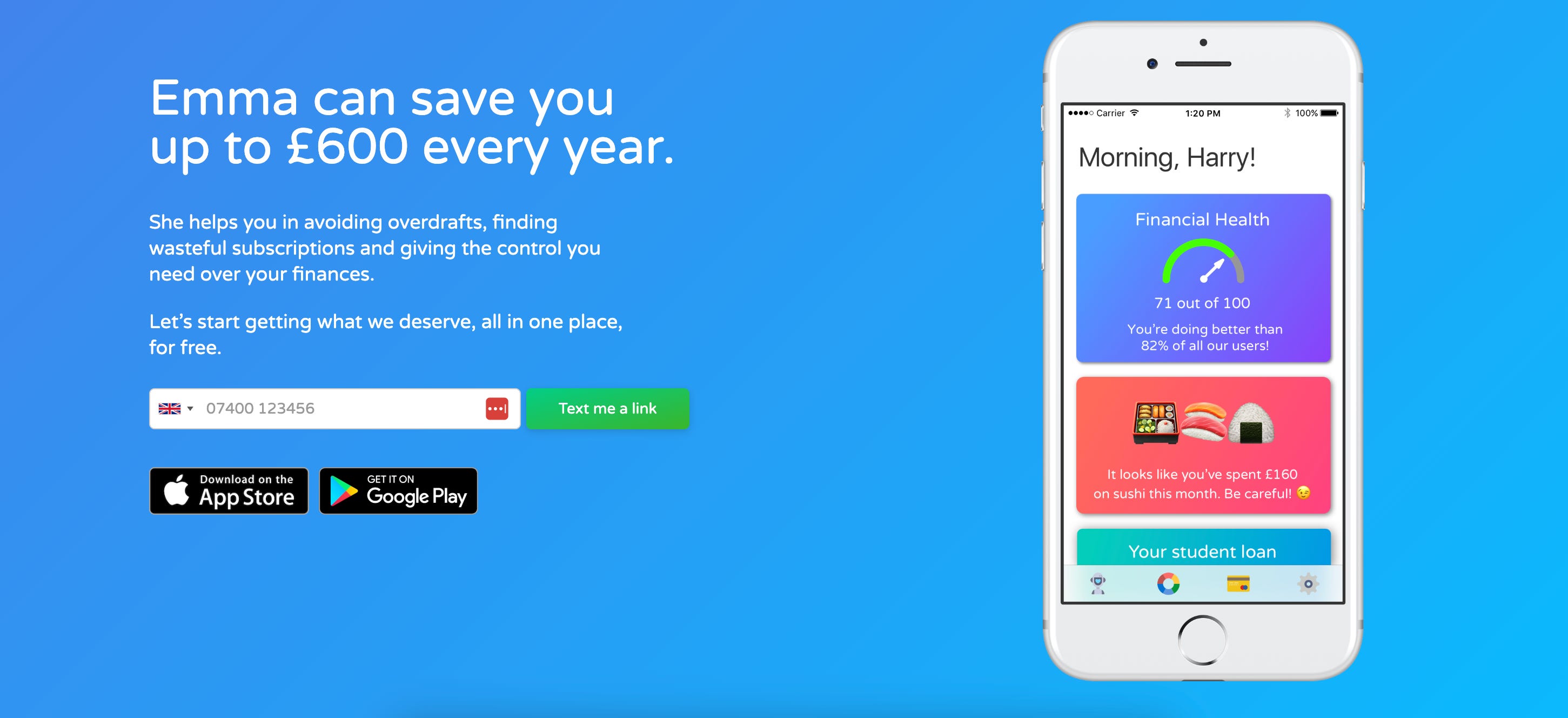

EM: When we started, it was a budgeting product. It helped you connect your bank accounts and then just budget. Now it’s becoming basically the financial control center of your life.

JB: Can you be more specific? What does Emma actually do today?

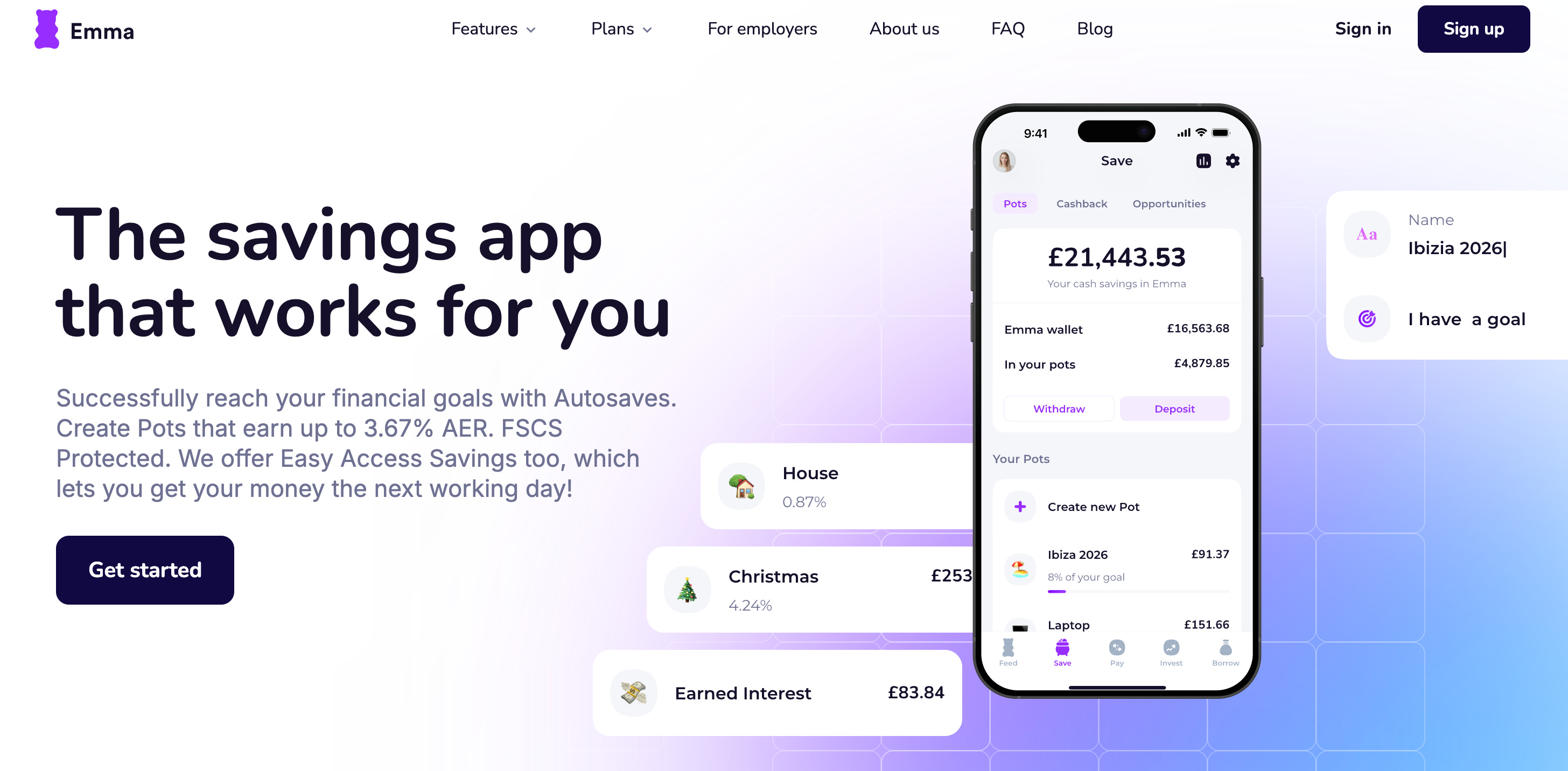

EM: We’ve got the core experience, which is the original one: account aggregation, budgeting, tracking your net worth, tracking your recurring payments, and being able to share some of your budgets with a partner or business partner.

On top of that, we provide savings products, so customers can actively save into the app and open savings accounts.

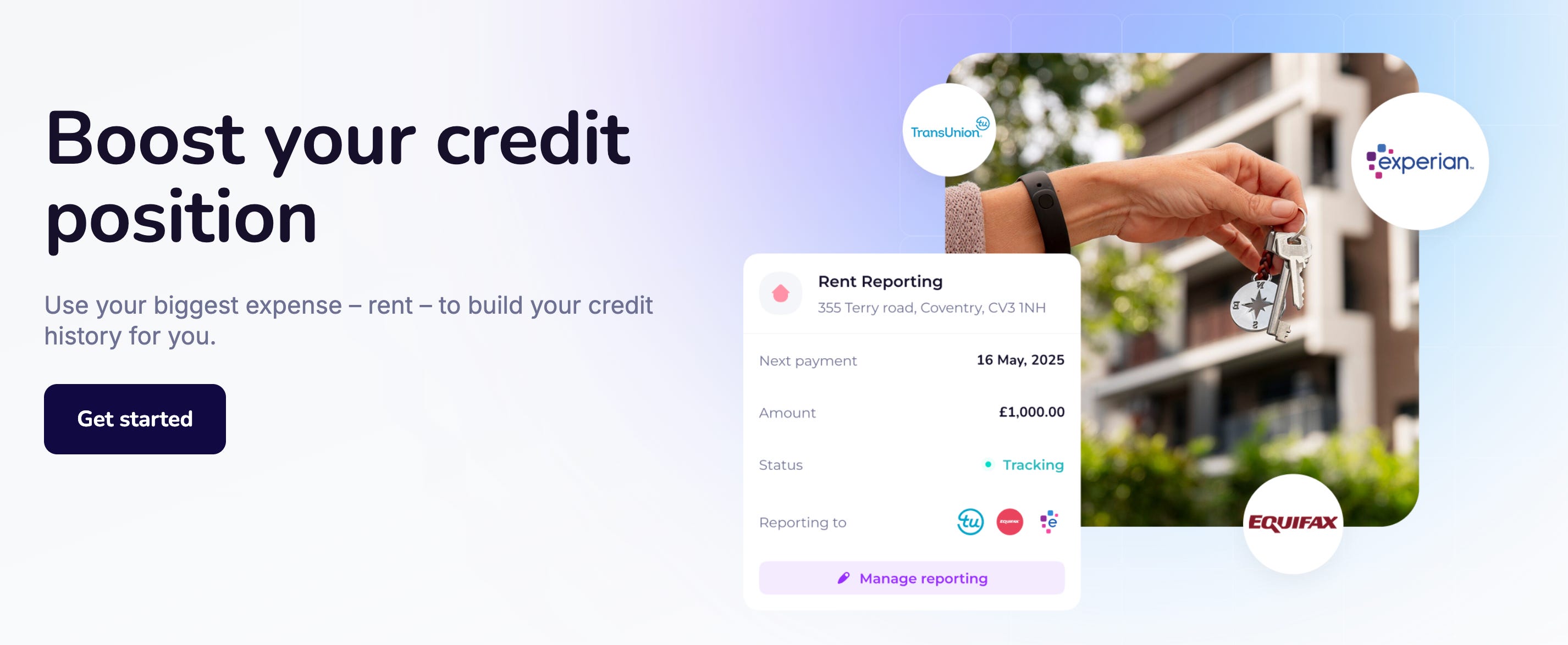

They can even set up roundups that transfer automatically into those accounts. We provide investment services. Right now customers can open up to two investment accounts in the app. And we provide tools to improve your credit score and credit report here in the UK. We have a specific feature called Rent Reporting that lets you report your rent payments back to the credit bureaus.

JB: Do you have credit monitoring in the app? Can you see your credit score in Emma?

EM: It’s coming next month.

JB: Are people depositing money directly into Emma accounts, or are you more of a marketplace introducing people to partner institutions?

EM: There was a phase, around 2019 and 2020, where we operated on an introducer-based model, referring people to external products. We quickly realized that model doesn’t work well for budgeting apps.

JB: What made you realize it wasn’t working?

EM: The credit card comparison model is a bit different. A site gets your credit score and credit report, and based on that, bombards you with loan and credit card offers. For a personal finance management tool, the customer’s intent is completely different. They’re downloading the app to track or budget their money, not to be spammed with loan offers. So that introducer model just doesn’t fit.

JB: Earlier you mentioned admiring Facebook for its social graph, but transaction data feels just as powerful. It tells you what people actually buy, not what they aspire to. Do you use that data to monetize Emma?

EM: We don’t really touch that data. For Emma specifically, we started in 2018, and it took us four years to figure out the revenue model behind the company. At the beginning, we thought we’d monetize with a subscription, but we didn’t have strong conviction in it. Two years in, we thought it would be comparison and switching, like we just discussed. After that, we thought it might be investments. Today we have very strong, high-level conviction that subscriptions are the right way to move these products forward, and the product is built around that now.

JB: What’s the pricing, and what’s the value proposition for someone to pay? There are a couple of other apps that let you track your accounts for free.

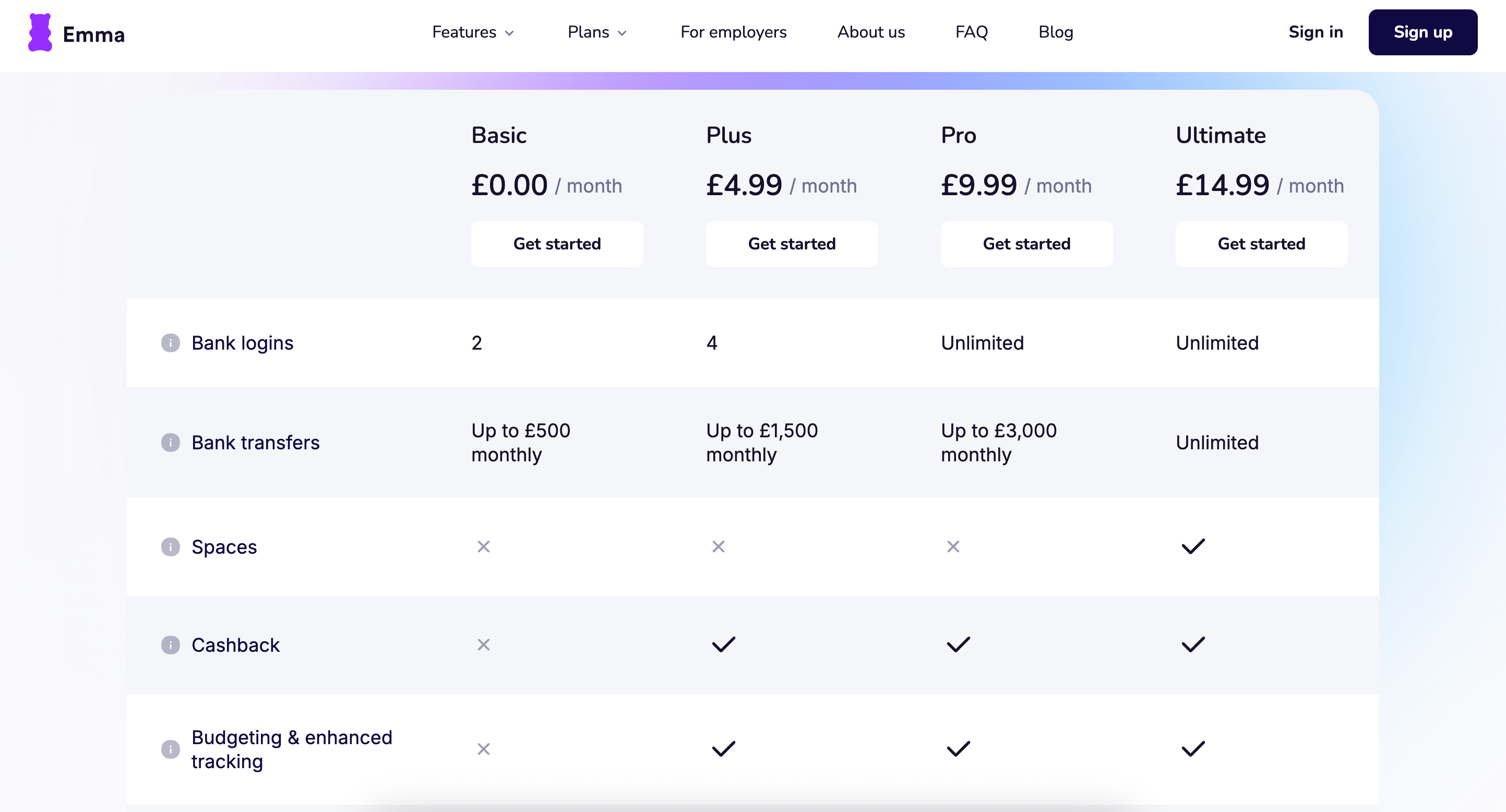

EM: We have three plans: Plus, Pro, and Ultimate. They’re priced at roughly 5, 10, and 15 pounds, though that varies by region. From a UK perspective, you pay a flat fee to access multiple services in one place: the core budgeting features we discussed, but also higher interest rates on savings accounts, lower fees on investments, rent reporting to improve your credit score and report, and credit monitoring will be part of these plans too. It’s basically a fixed flat fee that unlocks multiple services.

I still get reviews from people asking why they need to pay to save. That’s the dilemma of budgeting apps: why charge customers at all? But the reality is that’s the only way to make this work.

JB: I’ve seen online, and I’m not sure if it’s accurate, that you made 5.7 million pounds in revenue in 2024. Is that mostly subscription, or is there another split?

EM: Right now it’s around 90% subscription and 10% affiliate. That’s where we are today.

JB: How many users do you have, and how many countries do you operate in? What’s the scale of Emma today?

EM: In terms of paying subscribers, we’re in the hundreds of thousands. We’re live in the UK, where we have a fully fledged product covering everything from account aggregation to savings, investments, and credit score. We’re also live in the US and Canada, where you can download the app, but the product there is a bit different, just the core budgeting functionality for now. We’re hoping to bring the rest of it over in the next few years.

We actually have almost as many paying customers as free ones. There’s a very strong penetration on the subscription side, but that was a choice by design. We didn’t want to be like Duolingo, global with a tiny share of paying subscribers. Our internal split is closer to 50-50.

JB: How do you do that? Do you create friction, like limiting connections to two accounts on the free plan?

EM: Yes, there’s a lot of friction. Connectivity is limited, budgeting isn’t available on free, and there are several elements of the product that just aren’t on the free plan. That’s how we’ve structured it. To be honest, it’s very aligned with what we’re seeing in the US, where the last three or four products to launch in this space have actually launched as paid products from the start.

JB: Your first 100,000 users came with zero paid acquisition. What’s your acquisition model today?

EM: We’re heavily on paid social, mostly Meta and TikTok. We do a lot of video ads. The main reason it works is that we offer a seven-day free trial, so the payback period can be quite quick for us. At the same time, we still have a very healthy chunk of organic growth. Budgeting is something people talk about and search for, and we’re very dominant on those keywords.

We don’t do any influencer marketing yet, and we don’t do any branding. It’s purely performance-driven. We’re still at the stage where we need to focus on subscriber growth as fast as possible; brand recognition is something we’ll build over time.

JB: What’s your plan for the US and Canada? You mentioned it’s budgeting-only there right now, but you’re still selling subscriptions in those markets.

EM: The US is our next logical step. Bank integrations in the US have improved drastically over the last three to four years, mostly because Plaid built partnerships with essentially every bank. So you get an experience there that’s very similar to the UK for the major banks.

Canada still has the issues you mentioned. Banks like Tangerine still enforce two-factor authentication that locks customers out every other day. There’s still policy work that needs to happen there.

JB: How do you position Emma in the age of AI, when anyone can use a tool like ChatGPT to build their own budgeting app?

EM: I don’t know if you saw it, but recently OpenAI announced ChatGPT-based finance tools. In the US, if you pay around $100 a month, you can connect your bank accounts and let ChatGPT analyze them. I’ve seen this pattern before in every product cycle: a big bank adds account aggregation as a test, and most of those tests fail over the years. I think the same applies to the OpenAI example.

Overall, we can’t afford to build software that makes mistakes anymore. The bar keeps rising, and even internally we put huge focus into making sure the basics are perfect, like transaction categorization.

We’ll also integrate AI into Emma. I think AI can help us take the next step in the product, things like proactive tips for customers and identifying patterns and trends. Even though these AI labs are shipping their own finance products, that doesn’t mean we can’t also use their models. That’s going to be part of our play, alongside a much bigger focus on actually taking deposits, moving beyond software and into holding money for customers directly.

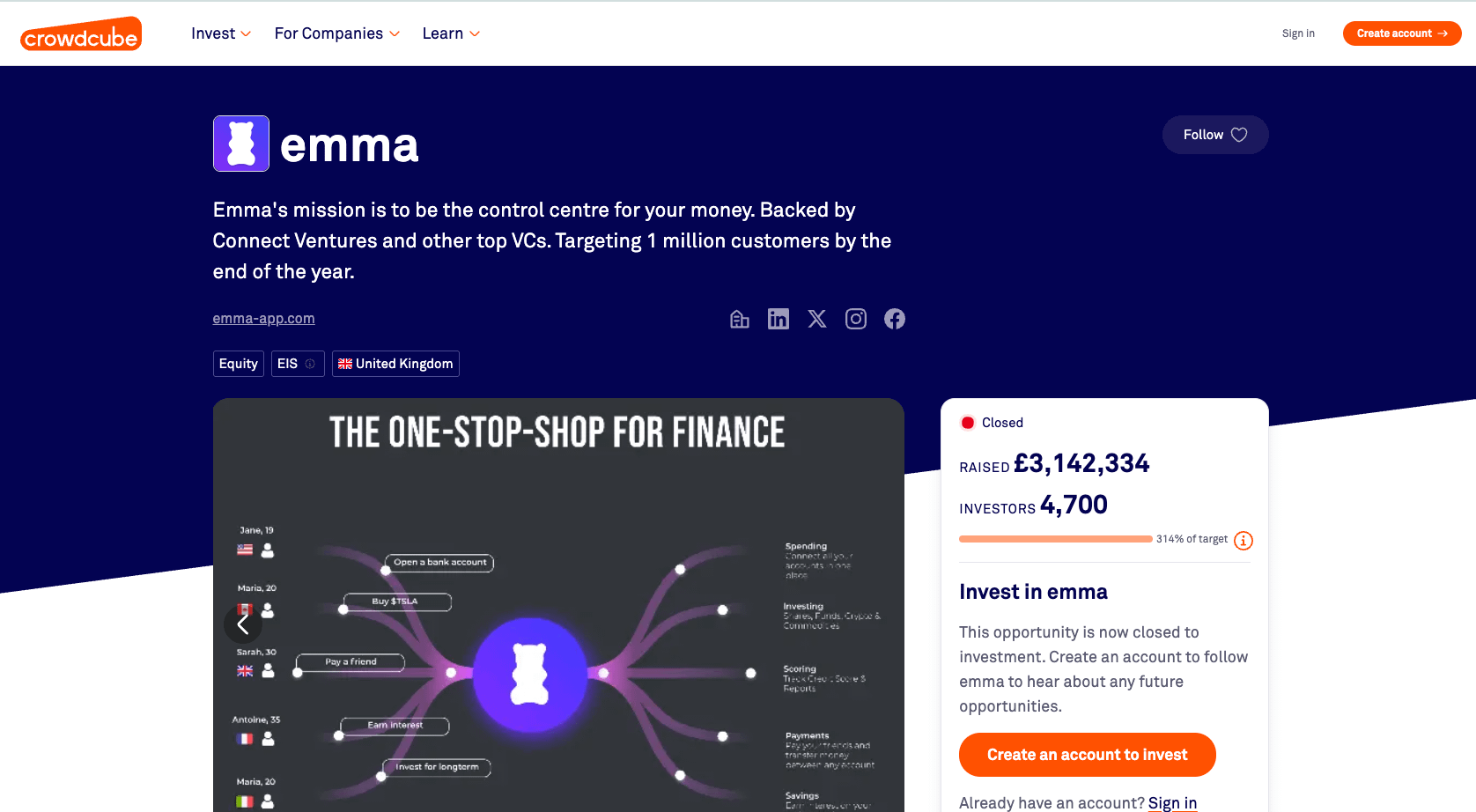

JB: You raised money through Crowdcube. Was that mainly a marketing asset, turning your users into owners of Emma?

EM: We’d already raised from institutional investors and angels, and then toward the end of 2021 we launched a crowdfunding campaign and raised money from about 5,000 people. That was a genuinely interesting experiment, and it happened right at the peak of the market, so we were able to raise a large sum.

JB: At what valuation, and how much did you raise?

EM: Around 3.2 million pounds, at a valuation of about 34 million pre-money. Those crowdfunding investors are still some of our biggest customers and biggest referrers.

JB: Does having thousands of crowdfunding investors create pressure to deliver an exit?

EM: You always want to provide a liquidity event for people at some point. But Emma has been growing quickly, our revenue has compounded year on year for the last three years, and we’re a profitable company, so we don’t feel any immediate pressure to exit.

JB: Looking back, what’s the decision that felt really risky at the time but now looks like one of the best calls you made?

EM: Putting up the paywall.

JB: Was that hard? Was there a lot of internal debate?

EM: For us it was four years of convincing ourselves that we needed to charge for what we were doing. The paywall in onboarding actually started a bit earlier, around 2020 to 2021, but the biggest decision was paywalling the bank connections themselves. That was the real turning point.

JB: So what does the free version look like now? Do you have to enter transactions manually?

EM: No. In the free version you can connect up to two bank accounts, and beyond that you need to pay. That decision took us about five years to make. We have a strange story in that we didn’t find our real monetization engine until four years in. So when people say “every day is day one,” for me, day one for Emma is actually the end of 2022, when we reset and decided exactly how we were going to build this company and where we wanted to take it. That completely changed our trajectory.

JB: How many employees do you have right now?

EM: Around 22 people, all based in the UK. We work from our London office Monday to Friday, in office, mandatory. I don’t think you can build a great consumer product in a fully distributed way.

We tried it during COVID and it was a mess. If you want to craft something well, everyone needs to be in the room, able to talk to each other fast, whether that’s customer support flagging a bug, engineering shipping the fix, or marketing advertising the feature, all in the same room.

JB: Did going remote during COVID cause real problems?

EM: Right after COVID we went fully remote and hired a bunch of people outside the UK. Then at the end of 2022, our “year zero,” we decided to bring everyone back in. We did a progressive rollout: people in London were first asked to come in two days a week, then three, then five. Anyone fully remote was transitioned out over time. Now all our job openings are London-based, in-office, and we don’t hire remote anymore.

JB: Looking at Monzo’s last results, I noticed something like 70% of their new users came from referrals rather than paid acquisition. What’s your branding strategy, and how important do you think brand is to building a big business?

EM: I think brand matters once you hit Monzo’s scale. At that point it’s a completely different game. Right now we focus on zero branding. Our strategy is to win on customer acquisition first and think about branding later. It might be the wrong call, but we invest essentially nothing in branding and far more in acquisition, because we believe the product can speak for itself and we want people to use it, adopt it, and stick with it. I do think branding becomes a much bigger topic at a different stage of the company, once you’re approaching hundreds of millions of pounds in ARR.

JB: You mentioned being profitable, which means every pound you put into Meta or TikTok comes back through your paid model. How do you manage that budget?

EM: We’re probably one of the biggest advertisers in the UK market on Meta right now. We’re very aggressive. We like paid social and performance marketing. If you have a strong business model with a strong payback period, there’s no reason not to lean hard into performance marketing. It’s working really well, and we want to build a big business driven by performance. That said, I think this changes as you scale, because these channels eventually hit saturation, where you’ve reached everyone and no one new adopts the product. We’re still very far from that point. I think brand starts to matter more once you’re closer to that kind of ceiling.

JB: Emma was founded in 2018, and you’d been experimenting with budgeting apps since 2017, but you’ve said you really feel the business has existed since 2021, when you put up the paywall. If you could go back and give yourself advice at the beginning of Emma, what would you say? What’s the thing you wish you’d learned faster or cheaper?

EM: Business model. I came straight out of university with that mindset of “build a business without a business model and just grow as much as possible.” But the reality, especially in Europe, is that investors overwhelmingly fund B2B. It’s probably 95% B2B, 5% B2C. I went to multiple fundraising rounds with a B2C product and no business model, and that made the conversation extremely difficult, even though our metrics looked great, my co-founder looked great, and the product looked great.

Monetizing from day one makes that conversation much easier if you’re building B2C. I don’t think there’s any other free product out there without a revenue model attached anymore. That was the biggest problem we had early on, and it’s the thing I’d do differently right away: think about scaling and distribution from day one, because that’s the most important thing.

We were fresh out of university, we were engineers, and we were thinking about building features. Emma has something like 350 different features at this point. We’ve built every power-user feature you could ask for, but features don’t drive growth the way you’d think. Maybe a couple of them help with engagement and retention, but they’re not as fundamental as having a strong business model and a strong distribution model.

JB: In the next three to five years, what would the best-case scenario look like for Emma?

EM: If Emma can be live across the UK, US, and Europe with millions of subscribers, that would be a great achievement. We’re also well positioned with AI, and well positioned to launch a B2B proposition.

JB: What would a B2B version look like? Something for employers, or insurance plans?

EM: I think we can help businesses structure their money in ways others can’t, because we have deep know-how from doing it so well for individual consumers.

JB: So Emma would be used by businesses themselves, not just bought by businesses and handed to employees? What would you actually launch in B2B, accounting software?

EM: There’s a huge space of decaying incumbent software, Xero and QuickBooks, that I think needs to be challenged, and I think Emma can challenge it.

JB: That was Edoardo Moreni, co-founder and CEO of budgeting app company Emma. Thanks for listening to my show. Make sure to follow Fintech Growth Insider on Apple Podcasts or Spotify, so you never miss a new episode. And if you are interested in stealing proven growth tactics from your fintech competitors, please sign-up to my newsletter on fintechgrowthinsider.com